The Evolution of Loyalty: Loyalty Programs are already changing

Technology has driven fundamental changes in Customer behavior and how they shop. Today, Customers search for products, seek thoughts and opinions of other Customers, and increasingly order and pay for items online and via apps. Customers are also commenting on social media and even playing online games to earn virtual rewards. Thus, retailers have increased opportunities to listen to Customers and connect with them to deliver added value and help meet their needs at every touch point. For example, we can recognize our loyal Customers and drive engagement by providing advice on wine pairings, for example, or thanking them for posting a review and surprising them with a personalized offer while they are shopping online. By tracking and rewarding interactions beyond spend, we obtain a deeper understanding of our Customers to build stronger relationships. It's about creating lasting connections through relevant rewards and experiences where and when Customers want them.

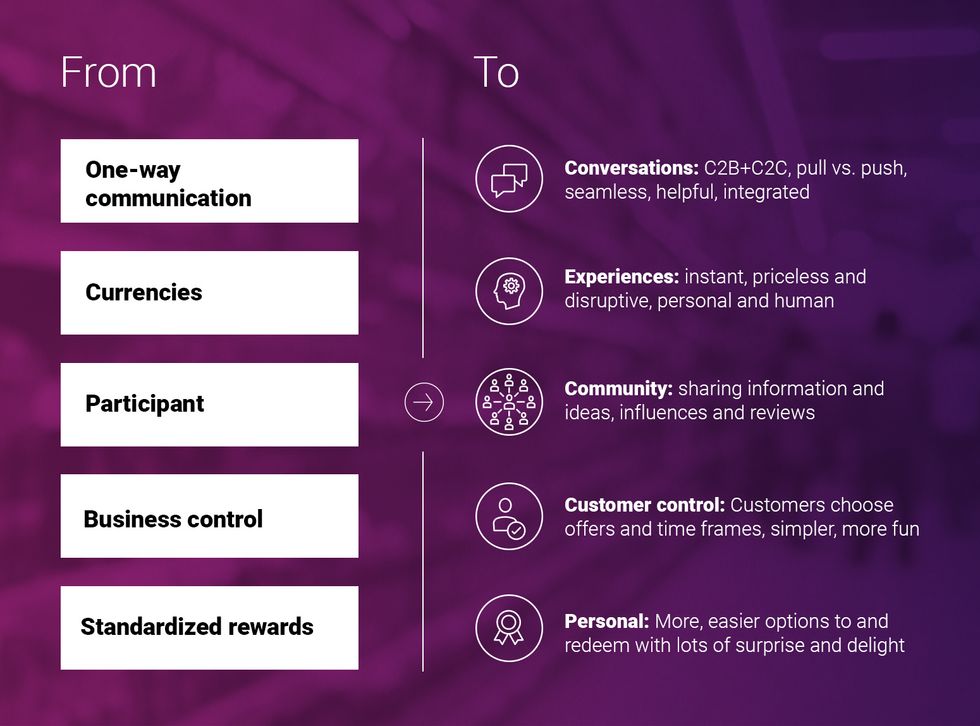

The evolution is already underway, and the 'table stakes' have changed, as illustrated in this chart:

Foundational principles for developing a brilliant loyalty strategy

Below are principles to follow to develop a successful loyalty strategy:

What to Avoid

Although loyalty programs have been around a long time, many of them still have fundamental limitations.For some consumers the rewards are not worth the effort to participate in the program. For others, the requirements of participating are inconvenient, such as showing your card to earn points or getting paper versus digital rewards. If the proposition is too complex, busy Customers will just opt out. If reward thresholds are too high, it may take too long to earn a reward so Customers may just stop give up.Below are program pitfalls to avoid:

- Low relevance for Customers

- Low perception of generosity

- Barriers across the Customer experience

- Reward/tier thresholds that are too high

- Developing a complex proposition which is difficult to understand

- Treating the program just as a promotional tool

- Having partners lack appeal or relevance

- Requiring too much effort for the Customer to participate

A Look to the Future

Programs designed today should consider emerging trends to be relevant into the future. Below are my thoughts on what to expect:"Digital" and "omni-channel" are outdated termsBoth have been buzzwords in recent years, and with good reason. Customers own an average of 3.4 devices, and think of themselves, of course, as one person who just naturally integrates several modes of connection. Retailers and brands must recognize and interact with their Customers across all channels cohesively; 53% of Customers expect this right now, an expectation that grows exponentially every digital moment.Accordingly, a separate 'digital' or 'omni-channel' strategy is meaninglessBoth are elements of a larger Customer strategy, or as simple communication channels / executions within the loyalty or marketing strategy. Companies who have separate initiatives or departments focusing on digital or omni-channel are already almost hopelessly behind the curve. If your digital marketing strategy is different than your brand marketing strategy or your Customer Strategy, you are in big trouble.Also becoming outdated are "points"Points are becoming increasingly implicit within loyalty programs. Programs' messages should focus more on the actions and rewards, rather than the point process within the program. Lately, best practices are really recognition and engagement programs that use 'softer' or implicit points within a loyalty proposition. As members make purchases within these type of programs, they receive more interactions, benefits, offers, and insider access, and those are the desired payoffs.Companies are targeting Generation Z as they become more active CustomersGen Z is coming into the spending picture more now at ages 12-23. The interesting thing about this age group is that they have never known a world without technology, mobile, and social. They are more tech-savvy and tech-demanding than other age groups. This will advance the mobile trends we have already seen in recent years, and require companies to pay even closer attention to their behaviors as they define their shopping identities.Customers want companies to demonstrate a commitment to doing goodAlthough not typically viewed as a component of loyalty programs, consumers are increasingly aware of companies' corporate social responsibility and it influences their opinions of brands. Corporate responsibility and philanthropy are nothing new, but it is now being incorporated into loyalty programs. Many programs today include charitable actions in their messaging, and more importantly to directly impact Customers, are offering opportunities for Customers to participate in charitable elements.. One example, members can choose donations to a relevant cause as a reward option.Customers co-create their own experiencesPerhaps the most exciting and interesting concept, and one that Customers truly appreciate, is the opportunity for Customers to create their own experiences. Tesco's former BuyaPowa proposition put Customers in the role of pricing managers – the more wine they encouraged their friends to buy, the cheaper the price was per bottle for everyone. Walmart enlists Customers to be new product developers and then category managers, driving innovation in new products. Canadian Tire's Customer-driven 'Tested' panel are de facto quality control experts. Even the constitution of Iceland was rewritten by its citizens, who contributed their thoughts for a better society in a social media campaign.

Measuring the Success of Loyalty Programs

There are many ways to measure loyalty programs– diagnostic measures that evaluate how well the program is being executed. Do you have awareness, appeal, and participation? Is the program driving engagement and increased loyalty among members? Stay tuned for Part 3: Measuring the Success of Loyalty Programs.

This is the ninth in a series of LinkedIn articles from David Ciancio, advocating the voice of the customer in the highly competitive food-retail industry.

brown round coins on brown wooden surface

Part 1: The Evolution of Loyalty

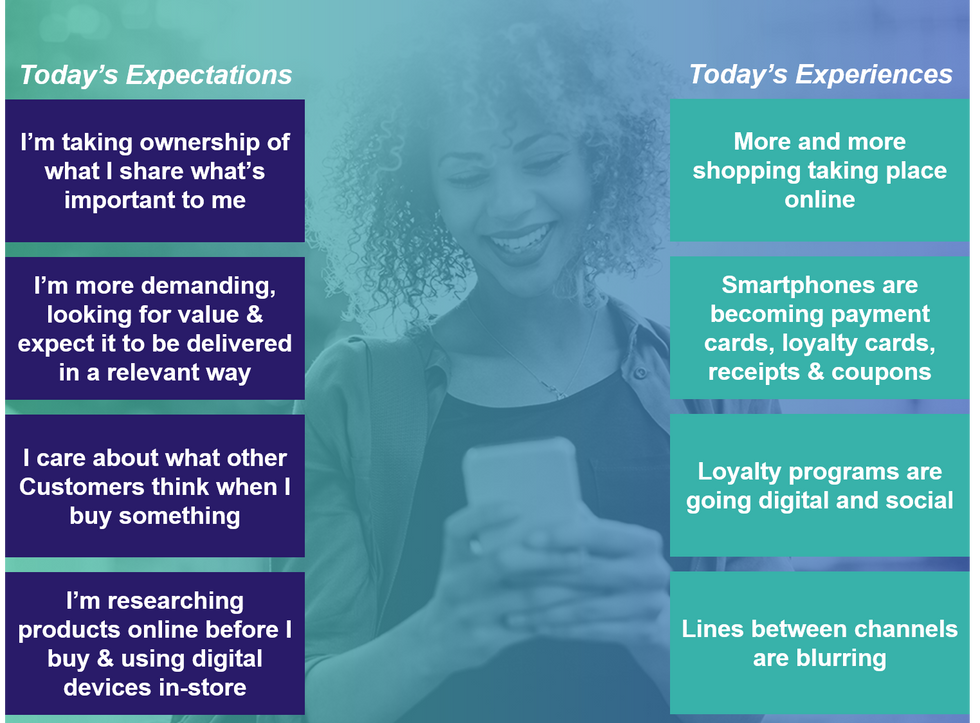

Today's 'always on, always connected' customers have become much savvier and discriminating. Unsurprisingly, they have lost their appetite for loyalty programs that deliver irrelevant offers and rewards via the same-old, tired propositions and experiences. Although the retail industry has generally graduated to 'loyalty 2.0' – more personalized communications, coupons, and channels based on data and segmentation science – the majority of loyalty programs are simply not keeping pace with the needs and expectations of today's shopper.

Customers now have much higher expectations of how rewards programs use of their gift of personal information – ever more valuable benefits and "hyper-relevant" experiences where and when the Customer wants it. Hence, the next (and long overdue) evolution of loyalty must no longer limit its focus to earning and redeeming, but also on continual and active Customer engagement. The 'program' must become a 'conversation' that creates interactions throughout the whole Customer journey to better demonstrate the retailer's loyalty to the Customer, and thereby winning incremental loyalty in return.

Customer Needs and Expectations Have Raised the Bar

Customers expect their experience with a retailer to be fully integrated and seamless across touch points. Whether they are searching for product information, checking reward status, making an online purchase or browsing in the store, they want to be recognized and have their needs understood and reflected in the retailer's offerings and the personalized service provided. Their lives are so busy, retailers who make shopping easier will be rewarded. Convenience and ease are key – whether it's making relevant suggestions and offers based on past purchases, making access to the rewards program fully digital, or offering an app that provides information, offers and payment options at their fingertips.

The following graphic illustrates how some of these expectations are playing out:

What This Means for Loyalty Programs Today and Tomorrow

The importance of a loyalty approach over a loyalty ‘program’

We live in an "attention economy" – Customers are attracted to offerings and retailers that win their attention in an otherwise cluttered and confusing multichannel world. Retail growth (and indeed, retail survival in a non-growth market) comes down to who best attracts meaningful attention. It's almost as if there are two choices that retailers face: win attention by being cheaper or by being more personally relevant (for Customers, this can be translated as better service, selection, convenience, etc.).

Arguably, in today's multichannel, post-recession world, the decision is binary and any middle position is short-lived and profit-starved. Being cheaper means competing in a continual race to the bottom against every type of price competitor and disruptor. Being more relevant means understanding Customers better than others, resulting in the ability to deliver an experience that Customers personally value. And, it means being more loyal to Customers than others are. In this way, a loyalty approach powers the growth strategy.

To earn loyalty rather than be given loyalty – to think of loyalty as a relationship earned through ever-relevant shopping experiences, offers, and conversations – is an important and powerful distinction with significant implications for any organisation in the multichannel world. One view puts the responsibility to change on the organization itself, while the other presumes that the Customer owns the change journey (from less loyal to more so). Only the former approach has been proven to drive sustainable growth, measured in organic, like-for-like terms.

Earning more loyalty means earning more sales – one more item, one more visit, one more customer, and so on.

Therefore, the essential question is around which type of loyalty program – points, discounts, surprise and delight, experiences, etc. – will best enable the practice of a loyalty approach? In our experience, the answer depends on how willing the business is to use data and insights to truly change the experience for its Customers.

Loyalty Trends and Best Practices

Customers have redefined what "relevance" means to them, rewarding retailers who deliver value and experiences that best meet both transactional and emotional needs. Clearly, today's customers are saying that points and discounts alone are insufficient. The most successful and appreciated loyalty propositions in practice today are focused on responding to the following Customer needs:

1) Sharing – Socially enabled and connected, local, advocacy and reviews, C2C and C2B. Customers expect propositions that listen more than talk, and marketing communications that speak with / on behalf of (not to) them. Think of propositions that help create communities, enable influence, ideas and reviews, and which enable Customers to gift their rewards.

2) Digital – Seamless omni-channel experiences, mobile enablers and connections. Customers expect programs that recognize them with or without a card and offers / status whenever and wherever they want. Integrate payment and 'discover' options.

3) Experiential – Experiences that are entertaining, fun, interactive, disruptive (the concept of gamification fits here), and priceless. Customers expect rewards for activities above just dollars spent and authentic 'thank you' messaging. Think of experiences that gratify instantly, are priceless and disruptive, personalizing and human.

4) Control – Of the offer, of time, of promotions and privileges. Customers expect transparency, simplicity, and curated choice. Think of experiences that are easier to enjoy and eliminate hoops.

Stay tuned for Part 2 coming soon: Foundational principles for developing a brilliant loyalty strategy

This is the eighth in a series of LinkedIn articles from David Ciancio, advocating the voice of the customer in the highly competitive food-retail industry.

Why shoppers today are different, and how retailers can weather the changes

Today's shopper is drastically different than even just a decade ago. Contrary to the 1980's and 90's, when incomes were on the rise and Customers were demanding high quality, premium items; the new millennium brought about stagnant incomes, the housing bubble and the Great Recession. As Americans faced the harshest and longest lasting recession since the Great Depression, Customers' attitudes, values, and preferences—particularly around money spend—had shifted greatly. The National Bureau of Economic Research (NBER) saw shoppers began saving by taking advantage of coupons, sales, private brands, and larger pack sizes, making more shopping trips, and shopping more at discount stores.

A key question coming out of the recession was, "When will shoppers return to their pre-recession behaviors?" In 2019, after five years of robust economic growth, does the data show consumers shifting back to pre-recession behaviors, or are the consumer changes more permanent?

To address that question, we will look at the three most interesting behavioral changes from the NBER report:

- Private brand sales

- Shifting to discount retailers

- Making more trips

Private Brand

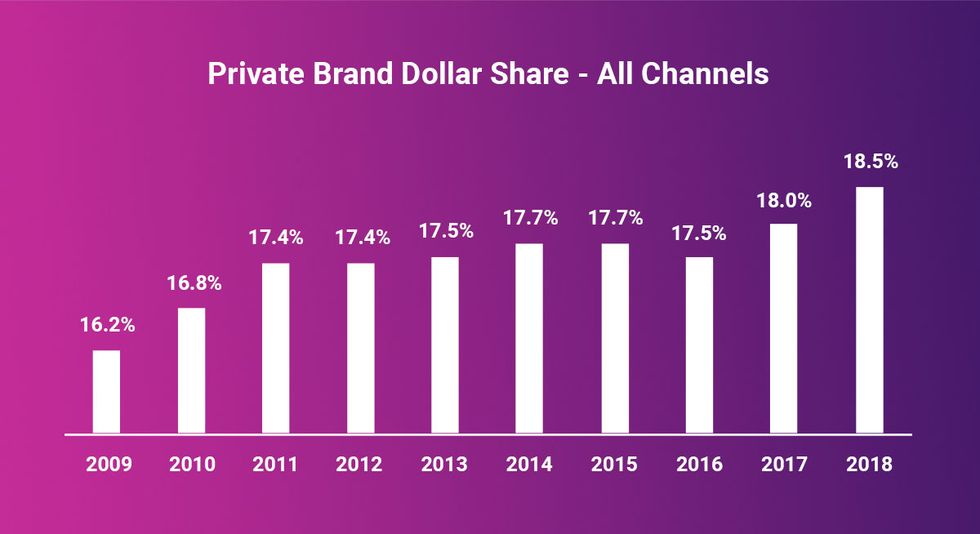

According to Nielsen, private brand's share of the market grew from 16.2% in 2009 to 18.0% in 2017 (source: Nielsen). This is a sizable chunk of the $682 billion grocery market (source: Nielsen TDLinx and Progressive Grocer).

Private brands have also grown faster than branded products from 2013-2017, when the private brand CAGR was 2.0% versus 1.2% for branded products. And the YOY number (2016 vs 2017) was 3.0% for private brand and -0.5% for branded products.

Discount Retailers

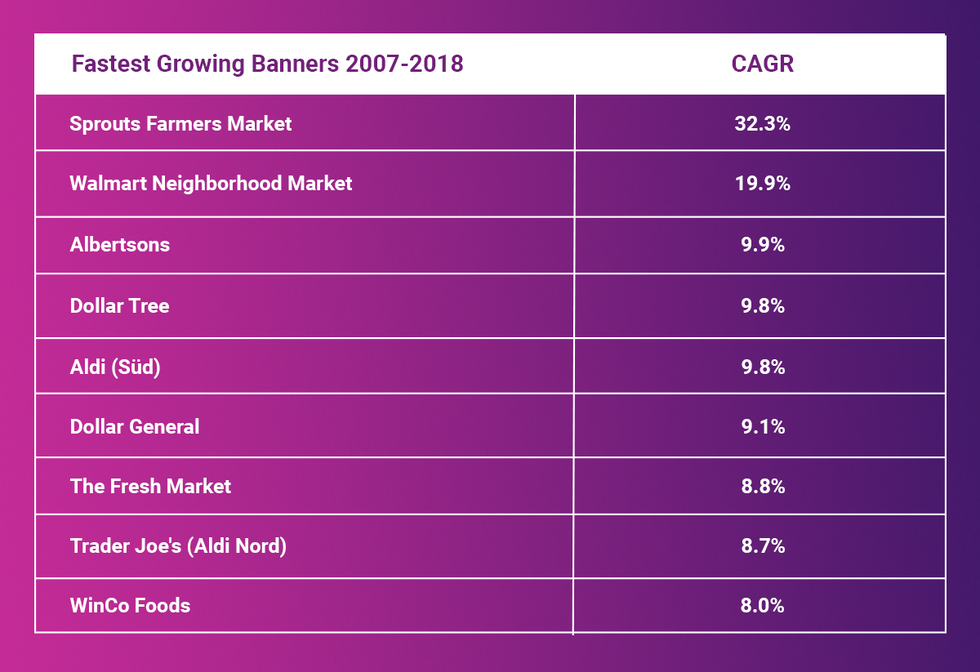

Looking at the top 10 fastest growing banners for grocery sales* since the Great Recession, five are price focused or discount retailers: Walmart Neighborhood, Dollar Tree, Aldi, Dollar General, and Winco Foods. Sprouts and Trader Joe's are not discounters but are known for the best prices within the premium segment. The Fresh Market is the only true premium banner, while Albertson's made the list because of an acquisition.

*(source: Planet Retail grocery sales. Filtered by banners exceeding $1 billion in 2018 grocery revenue)

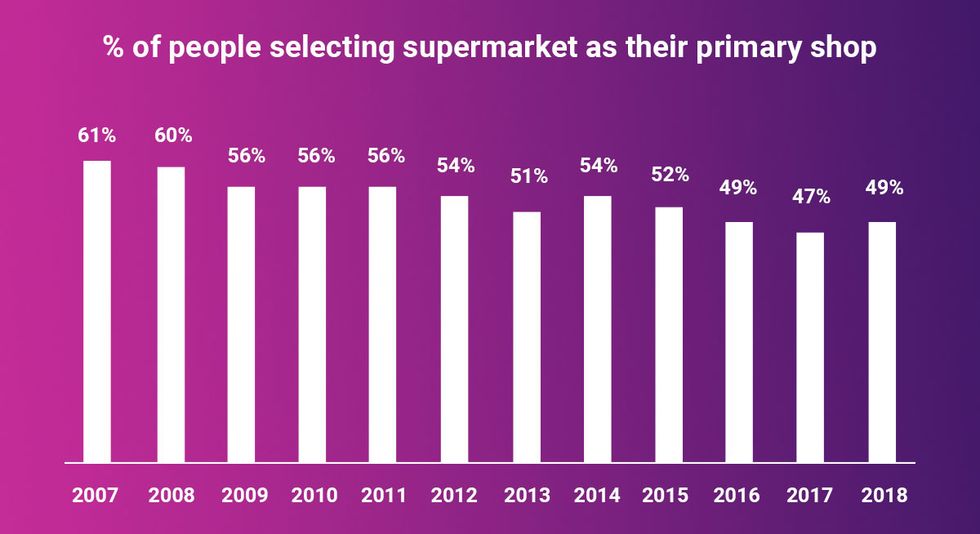

Moreover, since the Great Recession, fewer people define the traditional supermarket as their primary place to shop. FMI data shows a 12-percentage point decline since the Great Recession. And immediately following the 2009 recession, it dropped 5 percentage points as people explored lower cost channels.

More trips

More trips opened the door to visiting multiple retailers, allowing shoppers to find their preferred combination of price, quality, and store experience. In recent years, visits have fallen somewhat, but the number of channels and retailers visited continues to grow, according to the Food Marketing Institute (FMI). In fact, it's grown by almost 20% since 2015. Moreover, FMI, along with dunnhumby's RPI, finds that the average household visits about four different retailers in a month (source: FMI Grocery Trends 2018).

When will pre-recession behaviour return?

The evidence suggests that much of this price-conscious behaviour continues into 2019 and will likely persist for many more years. Private brand will likely continue to strengthen as Aldi, Lidl, Costco, and Trader Joe's continue growing. Many retailers are realizing that a strong private brand is key to their success, as it drives differentiation, improves value perceptions, and builds the overall retailer's brand.

Shoppers are also likely to continue shifting toward discounters, particularly for the commodity categories and items. Ecommerce will also make it easier by buying commodity items from low-cost providers. Lastly, Brick and Mortar visits could continue to fall as Ecommerce gains share and shopping multiple banners will likely continue as the market continues to fragment and specialize.

What does this mean for traditional supermarkets?

The key takeaway? We think about value differently since the Great Recession. Perceived value is the combination of our perceptions of quality and price. Before the recession, value was driven more by quality, but since the recession, it's driven more by price. Quality is still important, but when deciding to take action, retailers must carefully consider how those changes will impact price perceptions.

For example, many regional retailers think they can differentiate themselves by moving more upmarket, either more premium and/or more natural/organic. Still others think that becoming more digital and multichannel is the answer. In both instances, retailers should understand how these changes will impact both quality and price perceptions. In today's post-recession market where shoppers' price anchors are increasingly influenced by Walmart, Costco, and Aldi, significant reductions in price perception must be countered by significant improvements in quality perceptions. Moreover, if a retailer's footprint covers lower, middle, and higher income markets, it is not likely that the quality improvements will exceed the lower price perceptions. If a retailer wants to move more upmarket, targeted real estate becomes essential for success.

This also holds for digital and eCommerce. Will the benefits exceed the costs? eCommerce often requires fees or increased prices to cover the incremental costs. Does the improvement in quality exceed the hit to price? Dozens of grocery retailers believe it does, while one of the most successful--Trader Joe's--recently cancelled their eCommerce pilot because they felt the added costs exceeded the benefits.

What can traditional supermarkets do to improve value perceptions?

The good news is that several factors can shape value perceptions besides investing in price. dunnhumby research finds that about one-third to half of a banner's value perception is impacted by base price – meaning that there are other areas that contribute. The most effective method is to layer lower prices with changes in assortment, merchandising, and store experience, and then tell your customers about these changes with carefully crafted messages.

The first step is to build a highly efficient organization. Efficiency and keeping costs low are essential for any retailer to compete in today's market. This is seemingly quite obvious but getting there can be painful. Labor is a big cost. Do you really need someone behind that counter? Trader Joe's, Costco, and Walmart are almost exclusively self-serve. How about ready-to-eat foods? This department can also be very costly, so do the benefits exceed the costs? Trader Joe's has minimal fresh prepared foods but fills that vacuum with high-quality frozen prepared foods that are easy to prepare. This reduces shrink and maximizes profit.

Of course, the pricing blocking and tackling plays a role. The high-volume items play a bigger role in price perception than the lower volume items. Are these higher volume items priced competitively? Could you increase prices on lower volume items? What about entry level price points or the minimum and maximum gap across the category? Lower entry price points and smaller gaps have both been shown to improve price perceptions.

Assortment and merchandising can also affect value perceptions. How much variety is on the shelf? Are there opportunities to simplify the SKU? Research has shown that too many choices can negatively impact variety perceptions and reduce the likelihood of purchase. How is the store merchandised? What products occupy endcaps? High volume, competitively priced items or less relevant overstocked items? What's at eye-level on the shelf? Is this filled with your key value items or expensive premium and natural/organic items? What do customers see when they shop your store?

Private brand is also a key element within assortment and is unique in impacting both quality and price. On the quality side, it can uniquely help differentiate the overall brand by providing products that can only be found at your store. They have your logo on them and are the quickest way to build overall brand equity. There is also an opportunity to aggressively price these items, defending you against the more price-focused banners. And once you have a strong private brand, those items can occupy your end caps and prime space throughout the store.

The fact of the matter is, today's consumers are different. So how can you adjust your value proposition to better align with the fundamental shifts? Of course, there is no silver bullet, but a review of which banners are succeeding, and which ones aren't, is a clear indicator of what works and what doesn't. In the meantime -- recalling a fictional storm memorialized in film -- we are clearly not in Kansas anymore. Nor are we likely to ever return. There's a new normal in retail, and the smartest players are adjusting to the realities. For more on who is succeeding, see our most recent Retailer Preference Index report.

Accordingly, business decisions are heavily based on experience, and more often on personal memory of choices and executions and how a thing has traditionally been done. As Chris Foltz, director of operations at Heinen's Fine Foods, told me, "Our industry, and our company, was very opinion-based, albeit expert opinions. We realized early on that we needed data on customer needs, customer satisfaction and customer buying behavior to improve our decision-making. As we adopted this metric-driven approach, I believe we prioritized our investments and effort to deliver a better customer experience."

These are a just few of the things that most retailers absolutely know for sure:

- We must acquire new customers in order to grow our business.

- Price-sensitive and "cherry picker" customers are not profitable. The competition is welcome to them.

- Customers are different in every region of the country. There are also differences between urban and suburban shoppers.

- Loyal customers are already giving retailers most of their spend in the categories offered.

- Weekly flyers and promotions always drive footfall and sales.

- After all these many years in the business, we know what customers want.

Why What We Know About Customers Just Ain’t So

The old axioms are no longer factual because customers themselves have dramatically changed, in their needs, expectations and experiences. Separating fact from fiction—and business truths from myths—will change how the business sees itself and how it will make decisions. The following are some of the new truths of retailing in the 21st century:

- Expanding share of wallet from customers who are already "loyal" can better optimize growth.

- Loyal customers need more love and investment than new customers.

- Retaining loyal customers and reducing churn among "opportunity" customers can drive more growth than acquiring new customers.

- Price-sensitive customers are often more profitable than other segments because their basket mix includes more private label products or higher-margin portion sizes.

- Behavioral "buy-o-graphics" and intended trip missions matter much more than demographics or geographics.

- Customer segments are typically distributed variably within geographic regions or zones, but all customer types exist in all stores.

- Store clusters built upon customer dimensions are more useful to operations and execution than store groupings based on geographic zones or volumetrics.

What We Know for Sure Can Fit on a Post-It Note

Agility in retail can only be maintained by understanding customers and using data in all available quantitative and qualitative forms. Here's a personal story to illustrate:

A perception-based research tool measured one retailer's progress against factors that customers themselves had said are most important to them. Before the first customer perception report was published, I set out to learn how the customer ranking compared to the rankings that the senior decision-makers would assign.

The regular weekly senior team meeting brought together many of the wisest and most seasoned leaders in the business. After briefly introducing the research methodology, I asked the team to list what factors they thought customers would list as important, and in what order they thought customers would place them.

Not surprisingly, each merchant tended to rank factors in their department higher on the list than those for other parts of the store. Although little agreement was reached, a compromise ranking was eventually defined.

Comparing our list to the customers' list revealed spectacular differences; leaders had listed most of the same elements as did customers, but in completely the wrong order. That day, the team experienced a true epiphany—they realized that "we didn't know what we didn't know."

The lessons learned were:

- Humility gained in discovering that "we don't know what we don't know" empowers the customer-first journey.

- To become more relevant to customers, we must become fact-based deciders and activators.

- Using customer data well creates true consensus and inclusive action.

In summary, “In God We Trust” ... all others must bring data.

David Ciancio is global customer strategist for Dunnhumby, a pioneer in customer data science, serving the world's most customer-centric brands in a number of industries, including retail. David has 48 years' experience in retail, 25 of which were in store management. He can be reached at david.ciancio@dunnhumby.com