people collaborating about smarter retail investments

Artwork courtesy of Roger Penwill

The inability to confidently diagnose also leads to a largely internal focus and a planning process that centers on marginally adjusting next year's spend, hoping next year will be better.

Over time, this internal focus can result in a disconnect with Customers and too much influence from external organizations with conflicted priorities. This Customer disconnect causes a misalignment between the evolving Customer needs and the retailer's value proposition, which opens the door for competitors and new market entrants. This was the case with Walmart, Trader Joe's, and Costco who have all significantly expanded their market share over the last 20 years at the expense of traditional supermarkets. Ironically, this also happened with discounters in the U.K, who now control over 12% of the grocery market.

If a retailer can confidently diagnose key issues and identify opportunities, knowing that performance will improve, they would be more confident reallocating available resources. More importantly, they will have the knowledge and information to scale back in areas less important to the health of the business.

"The essence of strategy is choosing what not to do." Michael Porter – What is Strategy, HBR 1996

However, reducing or reallocating resources is difficult for most organizations. Relationships, culture, and legacy are baked into many systems, processes, and activities that are simply disconnected from the Customer and the overall performance of the business.

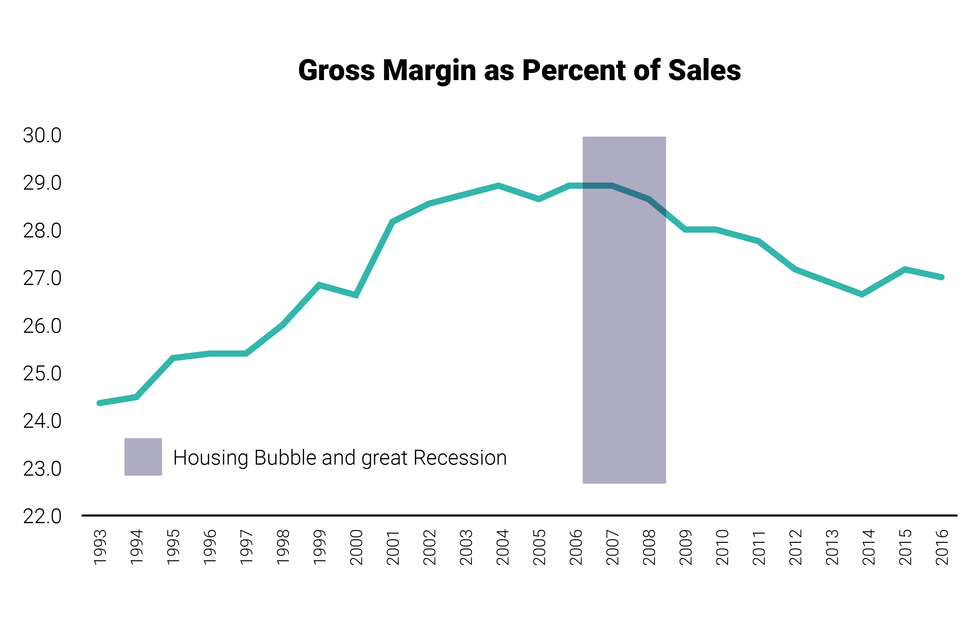

For example, many inwardly-focused traditional grocers failed to recognize the shift in the consumer and the market in the post-recession period. Looking at gross margins in the post-recession period, industry-wide gross margin as a percent of sales fell from 28.9% in 2007 to 26.7% in 2014.

U.S. Grocery Margin as Percent of Sales

Yet, other traditional retailers continued to incrementally increase their gross margins as they did in the pre-recession period, which may have helped them hit their short-term financial goals but damaged their long-term value perception. By 2006, Costco, Walmart and Trader Joe's had expanded into many markets and leveraged their strong value proposition in the post-recession period to steal significant share from supermarkets.

If traditional grocers diligently monitored the external market, changing Customer needs and diagnosed key issues, they might have responded by aggressively cutting back on expenses and investments. Consequently, they might have better managed the price perception gap and share loss over the long-term, rather than having to close stores today.

For example, a major retailer had a 2-percentage point gap in gross margin during the pre-recession market period and today it is over 5-percentage points. The premium price gap begins to reach a point where some retailers are simply no longer price competitive. Our research has shown that this lack of price competitiveness erodes not only financials, but also the emotional connection which used to be a strength for many regional grocers. Once the emotional connection starts to fade, it becomes increasingly difficult to win Customers and their wallets back.

So, how can retailers improve the ability to consistently identify key issues and take advantage of opportunities? It starts with a combination of people, process and data analysis to build the evidence-backed business case that can be used to develop a consensus across departments and alignment throughout the company. Depending on internal resources, this can include enlisting a partner like dunnhumby to help connect all available data sources, like Customer information from transactional data, market research, and online sources. In our upcoming Strategy posts, we'll look at strategic frameworks and other requirements to isolate key business issues and identify new and important opportunities.